Health Insurance in India: Cashless vs Reimbursement Explained

Health Insurance in India: Cashless vs Reimbursement Explained

Medical emergencies are unpredictable. One unplanned hospital stay can drain your savings in a matter of days. That is exactly why having the right health insurance plan is no longer a luxury — it is a necessity for every individual and family in India.

But buying a policy is only half the battle. Understanding how your health insurance actually works when you need it most is equally important. One of the most common areas of confusion among policyholders is the claim process — specifically, the difference between health insurance cashless vs reimbursement options.

In this blog, we break down both options to help you make smarter, more informed decisions

What Is Health Insurance and Why Do You Need It?

Health insurance is a contract between you and an insurance company where the insurer agrees to cover your medical expenses in exchange for a regular premium. Depending on your plan, it can cover hospitalisation costs, surgeries, diagnostic tests, pre- and post-hospitalisation expenses, and even critical illnesses.

In India, medical inflation is rising at over 14% annually. Without health insurance, a single serious illness could wipe out years of savings. A good policy ensures that a health crisis does not also become a financial crisis.

Understanding the Two Claim Methods

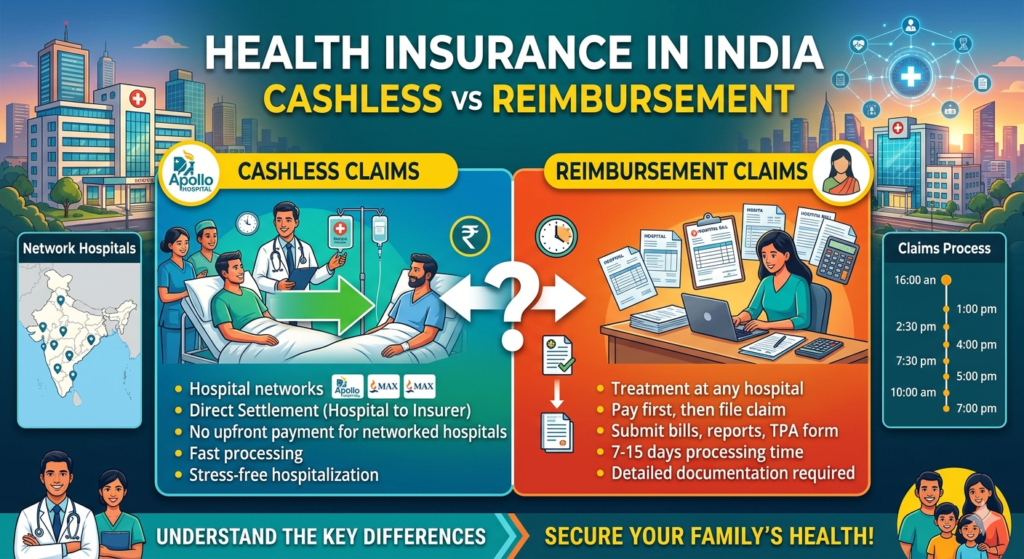

When you get hospitalised, your insurer offers two ways to settle your claim: cashless treatment or reimbursement. Both methods are part of your health insurance policy, but they work very differently.

Cashless Health Insurance: Pay Nothing at the Hospital

In the health insurance cashless vs reimbursement debate, cashless treatment is generally preferred by most policyholders — and for good reason.

Under the cashless facility, the insurance company settles your hospital bill directly with the hospital. You do not have to pay anything out of pocket (except for non-covered expenses). This is possible only at hospitals that are part of your insurer’s network hospitals list.

How it works:

- Get admitted to a network hospital

- Show your health insurance card or policy details at the TPA (Third Party Administrator) desk

- The hospital sends a pre-authorisation request to your insurer

- Once approved, the insurer settles the bill directly

The biggest advantage here is zero financial stress during a medical emergency. You do not need to arrange large sums of money at short notice. This is particularly helpful for planned surgeries or situations where the patient or their family cannot manage large upfront payments.

Reimbursement Claims: Pay First, Recover Later

In the health insurance cashless vs reimbursement scenario, the reimbursement route is often used when cashless is not available — typically at non-network hospitals.

Here, you pay the full hospital bill out of your own pocket first. After discharge, you submit all original bills, discharge summaries, and medical documents to your insurer. The company reviews the claim and reimburses the eligible amount within a specified time frame.

When is reimbursement useful?

- You received treatment at a non-network hospital

- Emergency hospitalisation at a facility with no cashless tie-up

- Certain outpatient or diagnostic expenses

The downside? You need to have immediate funds available, and there can be delays in getting the money back. Documentation must be thorough and accurate, or your claim may be partially rejected.

Cashless vs Reimbursement: A Quick Comparison

| Feature | Cashless | Reimbursement |

|---|---|---|

| Payment | Insurer pays hospital | You pay, insurer refunds |

| Hospital | Network only | Any hospital |

| Documentation | Minimal | Extensive |

| Financial stress | Low | High initially |

| Processing time | Faster | Slower |

Which Option Should You Choose?

For routine hospitalisation, cashless health insurance is more convenient and stress-free. However, having reimbursement as a backup ensures you are covered even at hospitals outside the insurer’s network.

When choosing a health insurance plan, check the size of the insurer’s network hospital list. A larger network means more opportunities to use cashless benefits. Also, look for insurers with a high claim settlement ratio — this indicates reliability when you actually need to file a claim.

Final Thoughts

Whether you go cashless or opt for reimbursement, what truly matters is that you are covered. Health insurance gives you and your family a safety net so that medical emergencies do not turn into financial disasters.

Understand the health insurance cashless vs reimbursement options, choose wisely based on your lifestyle and location, and always read your policy document carefully before you need to use it.

Stay healthy. Stay insured.